Smart glasses drive 44% growth in global XR shipments

Thu, 26th Mar 2026

Global extended reality device shipments grew 44.4% in 2025, according to IDC, driven mainly by smart glasses.

The figures point to a marked shift in the XR market. As lightweight eyewear gained ground, shipments of virtual reality and mixed reality headsets fell sharply, suggesting demand is moving away from bulkier devices.

IDC defines extended reality as a category spanning virtual reality, augmented reality and mixed reality. In this market, smart glasses are devices that resemble conventional eyewear and may include audio, cameras and AI assistants, with or without visual displays.

Meta remained the clear market leader in 2025, accounting for 72.2% of global XR shipments. Its position was supported by its partnership with EssilorLuxottica, a broader smart glasses portfolio and new launches including an Oakley-branded eyewear line.

Even so, Meta's Quest headset range moved in the opposite direction. Shipments of the Quest line fell 42.3% year on year as supply chain issues combined with weaker demand beyond gaming-focused users.

Xiaomi ranked second with a 4.2% market share, driven largely by China. XREAL took 2.3%, centred on display glasses aimed at gamers, while RayNeo expanded its US presence through lower pricing.

ByteDance and Viture each held 1.5% of the market, though their trajectories differed. ByteDance shipments declined 30.5% year on year, while Viture shipments rose 94.9%, helped by retail expansion and a refreshed product portfolio.

Headsets decline

The numbers suggest XR is no longer defined primarily by headsets for gaming and immersive applications. Instead, a growing share of the market is tied to devices designed for everyday wear, especially smart glasses without displays, which already account for most XR shipments, according to IDC.

That shift has implications for companies competing in the sector. Vendors that built their XR presence around VR and MR headsets face a narrower market, while those with eyewear partnerships, broader retail reach or products linked to AI assistants appear better placed to capture current demand.

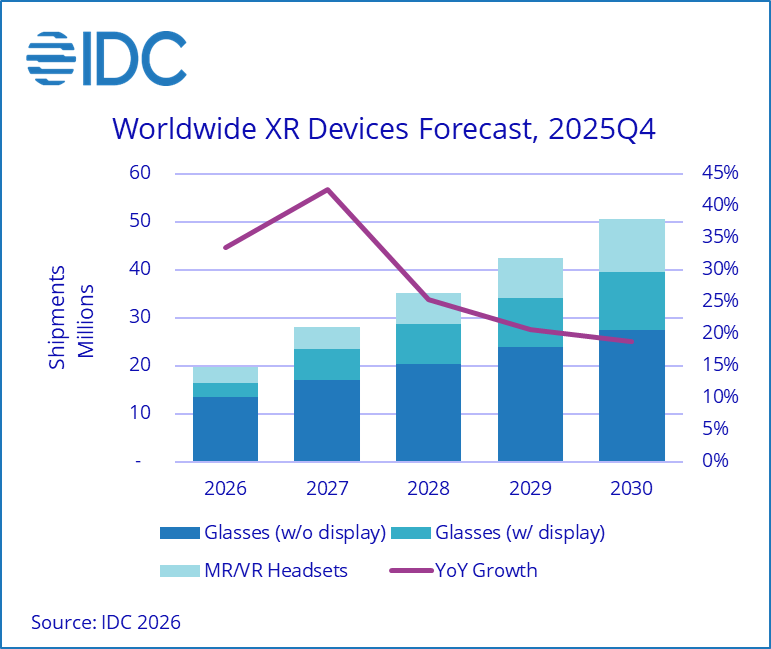

IDC expects the transition to continue through 2026. It forecasts XR shipment growth of 33.5% next year and projects a compound annual growth rate of 26.5% from 2026 to 2030.

In the near term, non-display smart glasses are expected to remain the main source of volume. By 2027, however, IDC expects display-enabled glasses to gain enough momentum to overtake VR and MR headsets in overall shipment volume.

AI and supply chains

The market's direction also points to a change in how device makers will differentiate their products. As hardware becomes thinner and lighter, software, services and onboard AI are likely to become the main points of distinction between rival devices.

At the same time, the sector still faces practical limits. The XR supply chain remains immature, with key components subject to intellectual property constraints that limit competition and may slow hardware development.

Those conditions could make it harder for manufacturers to stand out through component advances or industrial design alone. In that environment, ecosystems and AI features may play a bigger role in shaping demand than the hardware itself.

IDC also expects competition to widen as more companies enter the smart glasses market. That would broaden the contest beyond traditional hardware vendors to include the AI platforms and software layers that increasingly shape how the devices are used.

Jitesh Ubrani, research manager for IDC Worldwide Mobile Device Trackers, set out that view in comments accompanying the data.

"New products from Google's Android XR ecosystem, Snap, and a growing number of Chinese vendors will accelerate adoption by expanding smart glasses availability and familiarizing consumers with AI-first experiences," said Ubrani.